Johan Svanstrom is a man under pressure.

The Rightmove CEO came out swinging on Friday when his company’s latest set of annual results, for 2025, showed that they continue to harvest even more precious cash from its captive estate agent customers. Revenues were up 9%, average revenue per agent rose again to £1,631 and Svanstrom was bullish about the website’s future prospects, telling The Times later that it was ‘unthinkable’ that AI would replace it.

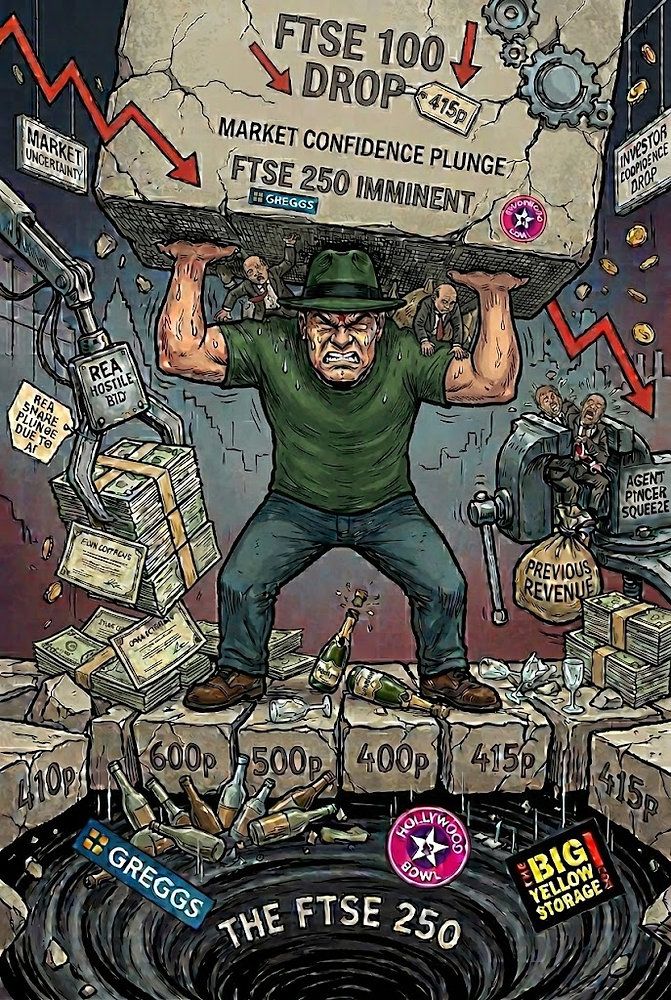

He also signalled that he intended to raise agent prices by another £120 per branch per month in 2026, in line with his target to get this to £2,000 average by 2028. Mortgage revenue also climbed significantly – up 46% to £6.8m – as Rightmove executed on Svanstrom’s plan to achieve £25m here by 2028. This pincer squeeze on agents – increasing costs whilst also taking revenue opportunities away – is having an outsize impact on smaller agents, who don’t have the sweetheart 70% RM discount deals that the corporates have nor the heft to generate mortgage deals at the same rate.

Rightmove’s shares bounced a little yesterday, up 4% in the day – mostly due to an unexpected extra £90m share buyback scheme, that cynics might position as more a market ‘bribe’ than anything strategically significant. But this doesn’t hide the fact that they’re still -46% down in the last six months. If it doesn’t increase a further 15% by Tuesday night, Rightmove will fall out of the FTSE 100 share index of the biggest companies in the UK, a huge blow to its prestige – and to the reputation of Svanstrom and his Board.

The market cap of Rightmove sunk as low as £3.15Bn this week, around half the amount that REA Group – owner of the ‘Rightmove of Australia’, realestate.com.au – bid for the business in September 2024, just 18 months ago. At that point, RM’s Board said that the offer of 775p per share (now 447p) “materially undervalued Rightmove and its future prospects”.

And it’s these “future prospects” that lie at the heart of Svanstrom’s problems. Markets – and investors – value businesses based on a ‘multiple’ of its current profits (and/or revenues) according to what they think the company can realistically look forward to generating in the future. High multiples indicate significant confidence – and REA’s offer valued RM at 22.5x its profit. Now? It’s 10.5x.

For context, the multiple that Svanstrom and co turned down valued Rightmove as if it was (Google’s parent company) Alphabet – now it’s more in the Biffa waste management category. A crappy outcome indeed (sorry, had to), but one that he is desperate to distract from.

That’s why he uses phrases like ‘unthinkable’ – because he doesn’t want you to think AI will replace Rightmove, he doesn’t want investors to think anything like this either and he certainly shies away from thinking about it himself. Yet that is precisely what markets are starting to price in.

When Svanstrom arrived with much fanfare on 6th March 2023 he would have been confident that his inherited share price of 440p would be a distant lowlight when his third anniversary came around. As it opened at 415p on Thursday the relentless pressure of maintaining the FTSE 100’s most-profitable company (70% margin v London Stock Exchange at 50% and InterContinental Hotels at 35% at second and third) must have been taking its toll.

It’s very unlikely that it will remain the FTSE 100’s most-profitable company by Wednesday this week, as it’s odds-on to drop out to the FTSE 250 - unless it can find +£300m in extra market cap in Monday and Tuesday’s trading. That would only really be possible if it was the subject of another takeover bid – and REA Group has its own -50% share plunge to deal with due to the same reason, AI. Other suitors are unlikely to ride to the rescue either, because the relegation will further depress market sentiment and make RM even cheaper due to ‘tracker’ funds having to automatically sell RM shares because it’s no longer a FTSE 100 stock.

As Svanstrom cracks opens the Crémant on his third anniversary at Rightmove next weekend, he’ll be getting used to a new life in the FTSE 250 alongside Gregg’s, Hollywood Bowl and Big Yellow Storage. This is a big moment – but also potentially a dangerous one for those who consider it a victory. As he has made clear with his ‘unthinkable AI’ comment, he is going to fight even harder to dominate the UK property industry in the decades to come.

Those that have been – and will be – hugely disadvantaged by RM’s relentless revenue rise, the ‘unthinkable’ needs to be thought. And planned for. And executed upon.

The pressure on Johan Svanstrom hasn’t evaporated with his £90m share buyback. For change in the property industry to be permanent, that pressure will need to be remain significant and unrelenting.

<path fill-rule="evenodd" cli